Introduction

Every year, thousands of shipping containers disappear at sea—around 1,390 on average. The financial impact is massive, with global shipping losses exceeding $4 trillion. And the risk doesn’t stop at ocean freight. Even land shipments face serious issues. In the U.S., nearly one in five large online orders, such as furniture or fitness equipment, arrives damaged or defective.

With risks at every stage of transportation, it’s no surprise that businesses rely on cargo and freight insurance. But many shippers still ask the same question: What do these policies really cover—and what’s the Difference Between Cargo and Freight Insurance?

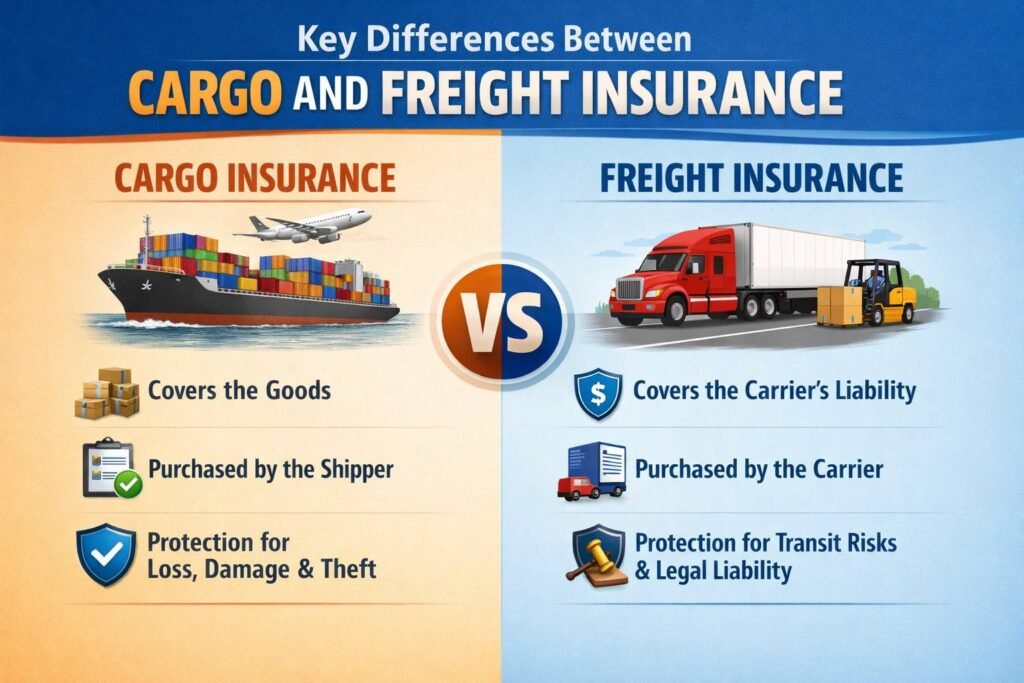

If you’re a seller, manufacturer, or freight forwarder, understanding this difference is essential. While cargo insurance and freight insurance both protect shipments, they serve very different purposes. Cargo insurance is designed to protect the value of the goods against loss, theft, or damage. Freight insurance, also known as freight shipping insurance, protects carriers and freight forwarders from liability claims.

As the global cargo insurance market continues to grow—from $71.4 billion in 2022 to an expected $106 billion by 2032—more businesses are clearly prioritizing shipment protection.

In this beginner’s guide, we’ll clearly explain the Difference Between Cargo and Freight Insurance, explore how cargo insurance and freight coverage works, and help you choose the right protection for your supply chain.

What is Cargo Insurance?

Cargo insurance is a type of policy designed to protect the owner of the goods being shipped. Whether your products are moving by truck, train, ship, or airplane, cargo insurance ensures that if they are lost, stolen, or damaged during transit, you won’t have to absorb the financial hit.

Think of it this way: every shipment carries risks. Goods might be mishandled at a port, damaged in rough weather at sea, or even stolen during land transportation. Without cargo insurance, the shipper—meaning you, the business owner—bears the full financial loss. With coverage in place, however, the insurance company compensates for the value of your goods, helping you recover quickly and keep operations running smoothly.

What Does Cargo Insurance Cover?

Most cargo insurance policies typically protect against:

- Loss of goods due to theft, accidents, or misplacement.

- Damage to goods caused by natural disasters, collisions, or mishandling.

- General average contribution, where shippers must share costs if cargo is deliberately sacrificed (e.g., thrown overboard) to save a vessel in distress.

Because of this broad protection, cargo insurance and freight solutions are often recommended for valuable or fragile shipments.

Who Needs Cargo Insurance?

Cargo insurance is especially useful for:

- Exporters and importers shipping goods internationally.

- Domestic shippers moving products across states or regions.

- E-commerce businesses sending large or high-value items.

- Manufacturers and distributors ensure their supply chain stays uninterrupted.

If your business owns the goods being transported, cargo insurance acts as a financial safety net. It ensures that unexpected shipping issues don’t disrupt your operations or cash flow.

What is Freight Insurance?

If cargo insurance protects the owner of the goods, then freight insurance is designed to protect the carrier or freight forwarder who is responsible for transporting those goods. In simple terms, freight insurance—sometimes called freight shipping insurance—covers the liability of the company moving the shipment, rather than the value of the goods themselves.

What Does Freight Insurance Cover?

Freight insurance usually provides coverage for:

- Carrier liability in cases where goods are lost or damaged due to the carrier’s fault.

- Limited compensation, often based on the weight of the shipment, not its actual value.

- Accidents or errors during handling, loading, or transport.

Because of these limits, freight insurance vs cargo insurance often becomes a key discussion point for businesses shipping high-value goods.

Who Typically Needs Freight Insurance?

Freight insurance is most relevant for:

- Freight forwarders and logistics companies managing shipments.

- Carriers and transport operators moving goods by land, sea, or air.

- Businesses seek limited protection when full cargo insurance isn’t required.

While freight insurance offers essential liability protection, it does not replace cargo insurance coverage. Understanding how cargo insurance and freight coverage differs helps businesses avoid assuming full protection where it doesn’t exist.

Cargo Insurance and Freight Insurance: Key Similarities

The terms cargo insurance and freight insurance are often used interchangeably, which can be confusing for beginners. Before diving into their differences, it’s helpful to understand where they overlap.

- Both policies are designed to protect goods in transit, offering financial coverage if shipments are lost, stolen, or damaged during transportation.

- Both can apply to domestic and international shipping, covering multiple modes of transport—whether by land, air, sea, or a combination of these.

Key Differences Between Cargo and Freight Insurance

When it comes to protecting shipments, both cargo insurance and freight insurance play important roles—but they’re not the same. Understanding the difference between cargo and freight insurance helps businesses avoid costly gaps in coverage and choose the right protection for their supply chain.

Cargo insurance coverage is designed for the owner of the goods. It covers the full value of the shipment against risks like theft, loss, or damage. Freight insurance, on the other hand, protects the carrier or freight forwarder. It covers their liability if something goes wrong during transit—but often with limited compensation.

To make things clearer, here’s a side-by-side comparison of the key differences between freight insurance vs cargo insurance:

Feature | Cargo Insurance | Freight Insurance |

Purpose / Policy Type | Protects the owner of the goods; covers full shipment value | Protects the carrier or freight forwarder; covers liability for lost or damaged goods |

Deductibles | Flexible; based on cargo value and risk | Usually fixed; may not cover full shipment value |

Premium Calculation | Based on shipment value, type of goods, and transit risks | Based on carrier liability limits, not cargo value |

Exclusions | May exclude improper packaging, prohibited items, or natural disasters | Broader exclusions; often excludes full cargo value |

Claim Process | Shipper files claim directly with insurer for faster resolution | Claims go through carrier; slower and limited compensation |

Legal Framework | Governed by insurance contracts favoring the shipper | Governed by carrier liability laws with capped payouts |

Risk Mitigation | Offers full protection for high-value or fragile goods | Partial coverage; shipper may still face losses |

Control Over Policy | Shipper controls terms and coverage | Carrier controls policy; limited input from shipper |

Subrogation Rights | Insurer can recover losses from third parties | Managed by carrier’s insurer; limited benefit to shipper |

Documentation Required | Invoice, bill of lading, insurance certificate | Proof of carrier liability and incident reports |

How to Decide Which Insurance You Need

Choosing between cargo and freight insurance doesn’t have to be complicated. By evaluating your shipment type, risk level, and business requirements, you can confidently select the right coverage to protect your supply chain.

Here’s a simple guide to help you decide:

1. Assess Shipment Type and Value

Start by reviewing what you’re shipping. If your goods are high-value, fragile, or shipped in bulk, they’re more vulnerable to damage or loss. In these cases, cargo insurance is the smarter choice. For smaller, low-risk shipments, the basic protection offered by freight insurance may be enough.

2. Evaluate Risks (Domestic vs. International Shipping)

Where your goods are headed matters. International shipments—especially across regions like Singapore, Malaysia, or China—face added risks like extreme weather, port delays, and customs issues. Cargo insurance offers broader protection in these scenarios, while freight insurance mainly covers carrier liability.

3. Check Regulatory or Contractual Requirements

Some trade agreements, client contracts, or shipping regulations may require cargo insurance for compliance. Always double-check your obligations to avoid penalties or disputes.

4. Work with a Trusted Provider

Partnering with a reliable provider ensures smooth claims and expert support. CargoInsurePro offers tailored insurance solutions for both domestic and international shipments across multiple regions—making it easier to protect your goods and your business.

5. Consider Combining Policies (Optional)

In some cases, businesses choose to combine cargo and freight insurance for full coverage. This approach protects the shipper’s goods and the carrier’s liability—giving everyone involved peace of mind.

Also Read: What is Cargo Insurance? A Complete Guide to Types, Benefits, and Business Needs

2 Responses